Certification in Machine Learning for Quantitative Finance

Advance your career in quantitative finance with applied machine learning

A structured professional Certification for quants, risk managers, portfolio managers, financial engineers,

data scientists and developers who want to apply machine learning to real financial problems.

| Next cohort start | September 21, 2026 |

|---|

Is the MLQF Certification right for you?

The MLQF Certification is designed for professionals and advanced learners who already have a solid quantitative foundation and want to apply machine learning to real financial problems.

A strong fit if you are

- ✓ A risk manager, asset manager, quant researcher, financial engineer or data scientist

- ✓ A finance professional with a strong mathematical background

- ✓ A developer or technical professional moving into quantitative finance

- ✓ A PhD or graduate student in mathematics, statistics, physics, engineering, computer science or economics

- ✓ Looking for mathematical rigor, applied Python work and finance-specific machine learning — not a generic data science course

This may not be the right fit if you are

- ✕ Looking for an entry-level finance course

- ✕ Missing the basics of linear algebra, calculus and probability

- ✕ Looking mainly for a short bootcamp or a lightweight online certificate

- ✕ Looking for a university degree or a purely academic master’s program

- ✕ Looking for generic AI, ChatGPT or business analytics training

Recommended background

To benefit fully from the Certification, you should be comfortable with linear algebra, multivariate calculus and probability. Finance and coding experience are helpful, but not required.

Not sure if you are ready?

Where can the MLQF Certification take you?

Traditional finance is becoming increasingly data-driven.

Quantitative roles require machine learning skills.

Generic online courses rarely provide a structured path.

ARPM helps bridge that gap.

The MLQF Certification helps you build quantitative finance, machine learning, portfolio construction, and risk management skills

that are relevant across several advanced finance career paths.

Not sure if you are ready?

Why professionals choose ARPM

Transition into quantitative roles

Qualify for advanced roles across the financial industry with deep technical knowledge.

Machine learning expertise for finance

Modern approaches beyond traditional financial engineering, focused on practical ML.

Flexible schedule

Fully compatible with a full-time job and personal commitments.

Practical infrastructure & Network

Access ARPM Lab, datasets, and projects, plus a global professional network.

Methodologies from leading teams

Learn directly from the methodologies used by top quantitative professionals.

Build a practical portfolio

Complete real-world projects reviewed and graded by human instructors.

Trusted by Leading Institutions

Corporate Partners

Academic Partners

Alumni Outcomes

What you will learn

The Certification is organized into two complementary tracks:

- Machine Learning - focused on statistical and machine learning methods (4 courses)

- Quantitative Finance - focused on financial engineering, risk management, and portfolio construction (3 courses)

The two tracks can be followed in any order and attended individually, depending on your background and objectives.

Courses in track “Machine Learning”

The courses in this track cover in depth the Machine Learning topics in the Lab, learn more

Mathematical Statistics for Finance Read more

Mathematical Statistics for Finance

Mathematical Statistics for Finance provides an in-depth discussion of the mathematical topics which lie at foundation of the applications of statistics to finance:

- The roots of the symmetry between the Mean-Covariance versus the Probabilistic Framework;

- The theory to learn from data in both frameworks.

More precisely Mathematical Statistics for Finance consists of the following parts of the "Data Science Map":

- The Probabilistic Framework describes the essential tools to operate in the Probabilistic Ecosystem, where:

- Statistical relationships among variables are modeled by probability distributions;

- Transformations among variables are non-linear;

- Structure is imposed via independence or more generally via conditional independence, which follows from the notion of conditioning.

- The Mean-Covariance Framework describes the essential tools to operate in the Mean-Covariance Ecosystem, where:

- Statistical relationships among variables are modeled by their mean-covariance equivalence classes;

- Transformations among variables are linear or affine;

- Structure is imposed via uncorrelation, or more generally partial uncorrelation, which follows from the notion of L² linear projection.

- Decision theory under risk addresses modeling and optimization of decisions under the assumption that the joint mean-covariance classes, or probabilistic distributions, of all random variables are known.

- Estimation leverages decision theory under uncertainty to learn, from data, relevant features of the joint mean-covariance classes, or probabilistic distributions, when these are not known. Key concepts include elicitability, asymptotic/random matrix theory, hypothesis testing.

- Inference covers how to learn not only from data, but also from subjective opinions, both mean-covariance classes (Black-Litterman) and probability distributions (minimum relative entropy).

Mean-Covariance Learning Read more

Mean-Covariance Learning

Linear Mean-Covariance Statistics represents the linear blueprint for Probabilistic Machine Learning.

It covers practical ways of learning observational and causal models from i.i.d. data samples and taking optimal decisions within the Mean-Covariance Framework.

The key ingredients are linear factor models, which model all mean-covariance structures: supervised (linear regression); unsupervised (principal component and factor analysis); hybrid (canonical correlation, total least squares); and causal (structural equation models).

This part also covers the estimation of linear factor models, namely mean/loadings and (high-dimensional) covariance matrices, in the context of financial applications.

This part covers the below portion of the "Data Science Map".

Probabilistic Machine Learning Read more

Probabilistic Machine Learning

Probabilistic Machine Learning discusses machine learning/artificial intelligence models, presented as generalizations of Linear Mean-Covariance Statistics.

It covers practical ways of learning observational and causal models from i.i.d. data samples and taking optimal decisions within the Probabilistic Framework.

The key ingredients are conditional distributions, which model all probabilistic structures: supervised learning (point and probabilistic); unsupervised learning (autoencoders and graphical models); and one-period reinforcement learning (causal Bayesian networks).

This part also covers the estimation of specific conditional distributions in the context of financial applications.

This part covers the below portion of the "Data Science Map".

Time Series and Reinforcement Learning Read more

Time Series and Reinforcement Learning

Time Series and Reinforcement Learning covers the dynamic counterparts of Linear Mean-Covariance Statistics and Probabilistic Machine Learning.

It covers practical ways of learning observational and causal models and taking optimal decisions in both the Mean-Covariance Framework and the Probabilistic Framework, when data is not i.i.d.

As such, this part includes multivariate econometrics, continuous time stochastic processes, and optimal sequential decision making.

This part covers the below portion of the "Data Science Map".

Courses in track “Quantitative Finance”

The courses in this track cover in depth the Quantitative Finance topics in the Lab, learn more

Financial Engineering Read more

Financial Engineering

Financial Engineering covers Steps 1-4 of the "Checklist".

Step 1 discusses how to price instruments across asset classes by means of the so-called risk-neutral or "Q" measure, as well as variations such as the CAPM or the APT.

Step 2 discusses how to convert raw financial data into well-behaved times series.

Step 3 discusses how to use econometric tools to model and estimate the evolution of such time series in the so-called real world or "P" measure.

Step 4 discusses how to map the future evolution of the time series back into the object of interest, which is joint distribution of the instruments future payoff.

This part covers the below portion of the "Quantitative Finance Checklist".

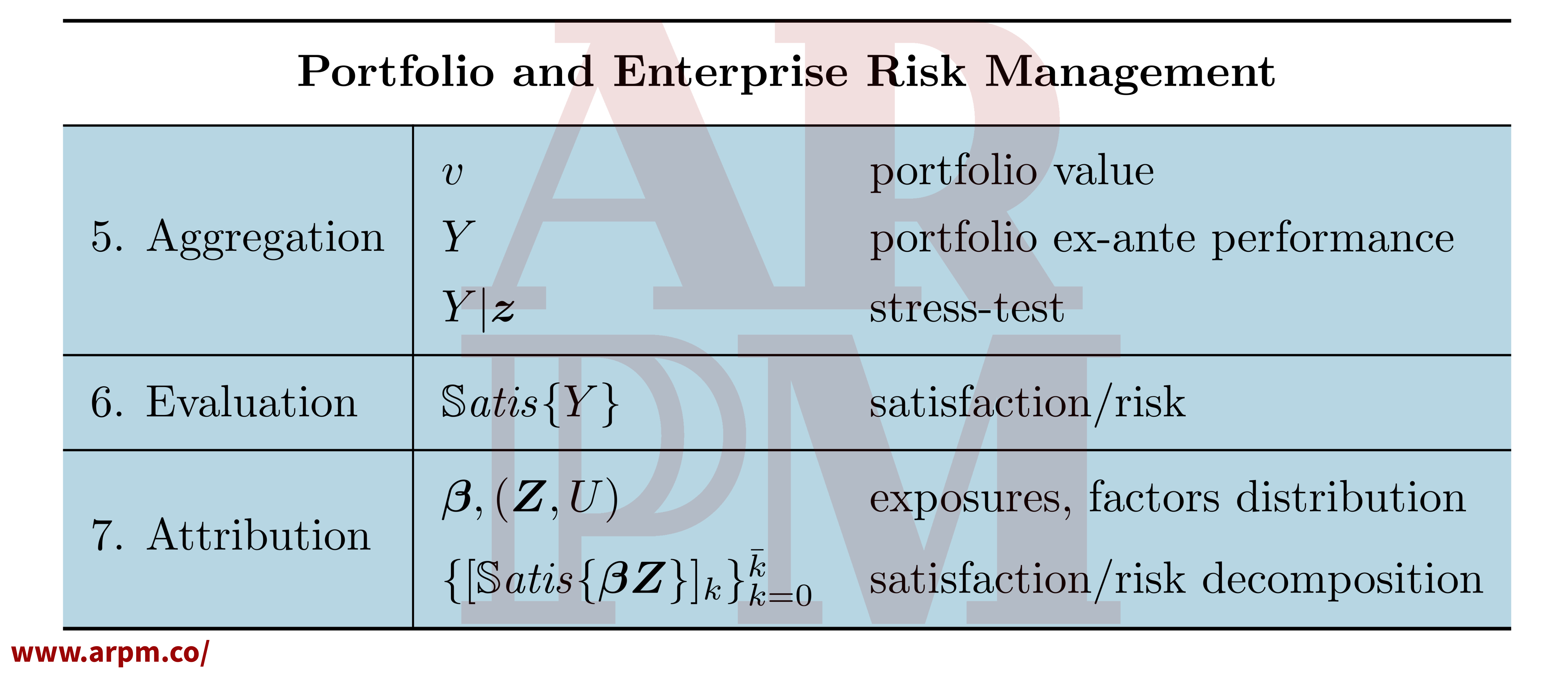

Portfolio and Enterprise Risk Management Read more

Portfolio and Enterprise Risk Management

Portfolio and Enterprise Risk Management covers Steps 5-7 of the "Checklist":

Step 5 discusses how to compute the aggregate value of a given portfolio, based on the portfolio's holdings; and how to aggregate the future payoff of each instrument into the future payoff of the portfolio under regular and stress market conditions.

Step 6 discusses how to assess the overall risk in a given portfolio at the fund, desk, or enterprise level.

Step 7 discusses how to attribute the overall risk to the contribution of different factors.

This part covers the below portion of the "Quantitative Finance Checklist".

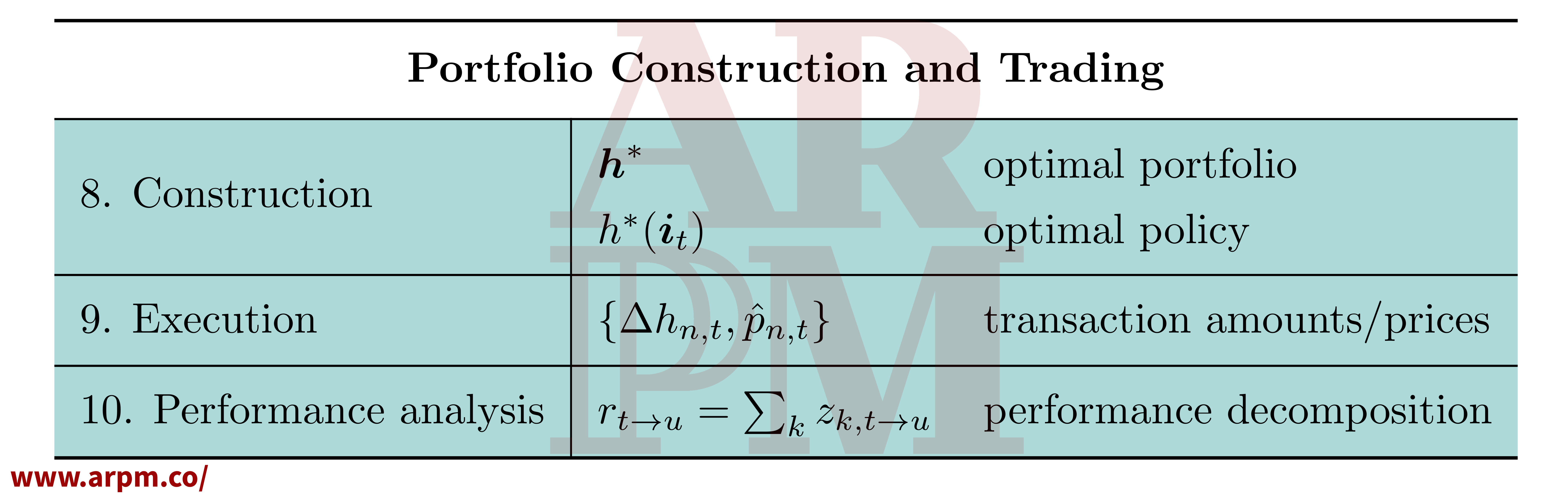

Portfolio Construction and Trading Read more

Portfolio Construction and Trading

Portfolio Construction and Trading covers Steps 8-10 of the "Checklist".

Step 8 discusses how to construct theoretical static portfolios based on mean-variance optimization or more complex algorithms; and to build dynamic investment strategies based on cross sectional heuristics or option based portfolio insurance.

Step 9 discusses how to implement a theoretical allocation in practice by optimally scheduling small orders in an electronic exchange.

Step 10 discusses how to assess past realized performance and attribute profits and losses to different contributors.

This part covers the below portion of the "Quantitative Finance Checklist".

Want to see how this program maps to your goals?

A professional certification built for applied quantitative finance

Unlike standard online courses, the ARPM Certification combines rigorous theory, applied Python labs, expert guidance, human-reviewed work, and a structured learning infrastructure.

| Feature | ARPM Certification | Typical Online Programs |

|---|---|---|

| Depth of Theory | Comprehensive and rigorous theoretical foundation | Usually focused on selected topics or modular content |

| Practical Code | Integrated Python applications in ARPM Lab | Exercises may be separate from the core learning path |

| Expert Interaction | Live sessions and access to expert guidance | Often limited to recorded content or forum-based support |

| Support | AI tutor plus human tutoring support | Support model varies by platform and course |

| Project Review | Human review of assignments and projects | Often automated, peer-reviewed, or self-assessed |

| Professional Outcome | Certification backed by applied infrastructure and assessment | Completion certificate based mainly on attendance/progress |

Learn from Attilio Meucci and the ARPM faculty

Directly learn from the methodologies used by leading quantitative professionals.

Attilio Meucci, PhD

Attilio Meucci is the founder of ARPM. He was the chief risk officer at KKR; the chief risk officer and director of portfolio construction at Kepos Capital; the global head of asset allocation for Bloomberg’s portfolio analytics; a researcher at Lehman Brothers; and a trader at Greenwich NatWest.

Attilio Meucci is the author of "Risk and Asset Allocation" – Springer and numerous publications in journals such as Risk Magazine, the Journal of Portfolio Management and the Journal of Financial Econometrics. He is the creator of the ARPM Lab.